The Grattan Institute released a report calling for a universal 15% loan fee to be added when student incur a higher education HECS/HELP liability. Reasoning behind a 15% loan fee is that it would go towards offsetting the interest-rate subsidy students receive as a result of their HECS/HELP liability being indexed at the rate of CPI (currently 1.3%). That is, a real rate of interest that is zero. As opposed to the Commonwealth Government actual cost of funding which is closer to 2.75% (current 10 year bond yield). In 2015/2016 this interest rate subsidy was around $550million for the year on total outstanding HECS/HELP liabilities of around $40billion. Bruce Chapman also wrote an article for The Conversation supporting the idea of a 15% loan fee.

Below are my reasons why a 15% universal loan fee is a far better idea than alternative proposals for reducing the funding burden of HECS/HELP. Not just the interest-rate subsidy that makes HECS fair for all types of students with many different backgrounds but also the implicit understanding that some students will fail to repay their HECS liability due to simple bad luck and the uncertainty of life. Continue reading

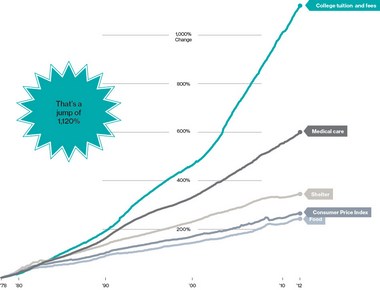

Source: Bloomberg, Data: Bloomberg Labor Department

Source: Bloomberg, Data: Bloomberg Labor Department